The banking industry is emphasizing algorithmic trading, which involves automated trades based on predetermined strategies determined by statistical models, even if regular investors are having a greater impact. The Indian stock market has undergone many transformations over the years. New trading strategies have emerged, the market pace has accelerated, and settlement times have decreased as a result of the fast digitization and integration of cutting-edge technologies. Let’s learn more about the strategies used in algorithmic trading.

What is Algorithmic Trading?

In algorithmic trading, a trade is made by a computer program that executes a predetermined set of instructions. The specified sets of instructions can be derived from any mathematical model, time, cost, or quantity. Algo trading eliminates the influence of human emotions on trading activities, which increases trading systematicity and market liquidity in addition to providing opportunities for profit for the trader. Theoretically, the deal can produce gains faster and more frequently than a human trader could ever achieve.

The concise definition can be:-

A sophisticated approach to the financial markets, algorithmic trading uses computer algorithms to carry out trading plans. Large volumes of market data are analyzed by these algorithms, which also spot trends and swiftly and precisely execute trades on their own. In the financial sector, this is being used more and more to help traders take advantage of market opportunities, control risk, and execute deals more quickly and efficiently.

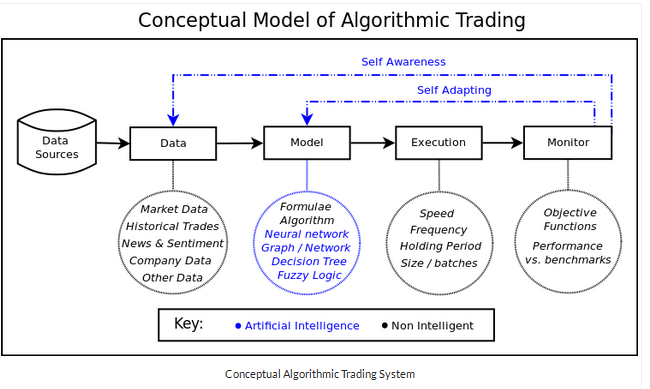

Components of Algo-Trade

The best way to understand algorithmic trading systems is to use a straightforward conceptual design made up of three parts: the trade execution handler, strategy handler, and data handler. Each part handles a distinct aspect of the trading system.

1. Data Component

Automated Data that is organized, unstructured or both can be used by trading systems. If information is arranged in a way that follows a predefined framework, it is considered structured. Spreadsheets, CSV files, JSON files, XML, databases, and data structures are a few examples. Trade volumes, end-of-day prices, and other market-related data are often accessible in a structured format. If there are no established structures guiding the organization of the data, it is considered unstructured. News, social media, videos, and audio are a few examples. Since this kind of data is more difficult to handle by nature, data analytics and data mining techniques are frequently needed to analyze it.

2. Model Component

An algorithmic trading system’s depiction of the external environment is called a model. Typically, financial models depict the way the algorithmic trading system thinks the markets operate. Any model’s ultimate objective is to be used to draw conclusions about the outside world—in this case, the markets. Although there are many different approaches and techniques that may be used to build models, they all ultimately accomplish the same goal: they reduce a complicated system into a manageable and quantifiable collection of rules that explain the behavior of the system in various contexts.

- Mathematical Models – Quantitative finance is the application of mathematical models to market behavior.

- Symbolic & Fuzzy Models – In symbolic logic, predicates are essentially evaluated to determine if they are true or untrue. Any given predicate can, to varying degrees, belong to the set of true and/or false predicates thanks to fuzzy logic, which loosens the binary true or false constraint. In terms of set membership functions, this is defined.

- Decision Tree Models – Decision trees and induction rules are comparable, with the exception that decision trees’ rules are structures rather than lists. The sort of decision tree that is generated depends on the characteristics of the training data.

- Neural Network Models – For algorithmic trading, neural networks are most likely the most widely used machine learning model. Layers of connected nodes between inputs and outputs make up neural networks. Perceptrons are individual nodes that are similar to numerous linear regressions, but they feed into an activation function that could or might not be non-linear.

3. Execution Component

The transactions that the model identifies must be carried out by the execution component. The functional and non-functional requirements of algorithmic trading systems must be satisfied by this component. The functional and non-functional requirements of algorithmic trading systems must be satisfied by this component. These specifications ought to be met by any algorithmic trading system implementation.

4. Monitor Component

Typically, objective functions are mathematical measures that measure how well an algorithmic trading system performs. One or more of these quantities would be “asked” to be maximized by the model component of the algorithmic trading system. This presents a problem because markets are dynamic. The models should be trained by the algorithmic trading system using data on the models themselves. This adjusts to shifting surroundings.

Impact of Algorithmic Trading on the Financial Market

Although algorithmic trading has greatly improved the financial markets, it has also generated new complications and difficulties that regulators, market players, and technology developers must carefully examine. The dynamics of global financial markets are still being shaped by the continued development of algorithmic trading.

1. Increased Market Efficiency

Because algorithms can execute trades faster and more frequently than humans can, they have increased market efficiency. This effectiveness is especially noticeable in extremely liquid markets where algorithms can react fast to shifting circumstances. In a time that is unthinkable for human traders, algorithms can evaluate market data, spot trading opportunities, and carry out orders quickly.

This swift execution speeds up price adjustments by allowing markets to quickly reflect new information. The latency of algorithmic trading systems is incredibly low, which reduces the amount of time it takes to send orders and receive executions. By reducing latency, trades are conducted at or close to current market prices, ensuring that prices in the market are current.

2. Increased Trading Volumes

Overall trade volumes have increased, partly due to the use of algorithms in trading. High-frequency traders and quantitative funds have been drawn to the market by the speed at which deals may be executed. Small price differences and market inefficiencies are exploited by high-frequency trading tactics, which significantly boost trade volumes. Algorithmic trading is being used more and more by institutional investors, including asset management companies and pension funds, to efficiently execute big orders.

Markets or asset classes are not the only ones where algorithmic trading can be used. A wide variety of financial products, such as stocks, bonds, commodities, and cryptocurrencies, can be operated by algorithms. A wider spectrum of traders are drawn to this diversity, which raises total trading volumes. Algorithms are skilled at carrying out intraday trading plans and profiting from brief changes in price. These tactics add to the overall growth in trading volumes because they require frequent trading.

3. Liquidity Provision

Market making is one example of an algorithmic trading strategy that increases market liquidity by continuously quoting bid and ask prices. This facilitates the buying and selling of securities by traders by reducing bid-ask spreads. Market makers constantly quote a financial instrument’s buy and sell prices. These quotes are automatically updated by algorithms in response to changes in the market, guaranteeing their availability and enabling traders to place and execute orders quickly.

Automated order matching is made possible by algorithmic trading systems, which rapidly match buyers and sellers according to preset standards. This effective order matching guarantees quick executions and maintains market liquidity. Algorithmic trading promotes more trading activity by lowering transaction costs and supplying liquidity. There is a greater willingness among market participants to buy and sell, which raises total liquidity levels.

4. Price Discovery

A key component of the price discovery process is algorithms. Algorithmic trading aids in the establishment of more precise and reflecting market pricing by quickly evaluating market data and spotting trends or abnormalities. Large volumes of market data can be processed in real-time by algorithmic trading systems. News, economic data, and other pertinent information are included in this. Fair market pricing is influenced by the speed at which algorithms evaluate and understand this data, allowing them to quickly adapt to new information.

Trend-following algorithms and statistical arbitrage algorithms examine past price patterns and trends. These tactics affect transient price changes and aid in the process of price discovery generally. Market participants can trade across exchanges and geographical areas thanks to algorithmic trading. A more integrated and effective price discovery process is facilitated by the speed with which information is reflected in prices across various markets thanks to the globalization of trade activity.

5. Risk Management and Automation

Complex strategies for risk management are made possible by algorithms. The possibility of human error is decreased by automated execution and risk controls, which assist in preventing errors and guarantee that trades follow pre-established criteria. Automated risk controls are a feature of algorithmic trading systems that help them monitor and reduce possible hazards. Predetermined characteristics including position limitations, maximum order sizes, and stop-loss orders are included in these controls. By taking these precautions, trading operations are kept within predetermined risk tolerances, and large losses are avoided.

Position sizes are dynamically adjusted by algorithms according to predetermined risk parameters, account equity, and market volatility. This optimizes the ratio of risk to return by enabling traders to scale their positions in accordance with their risk appetite and the state of the market. Take-profit and stop-loss orders are frequently incorporated by algorithms in order to control risk and lock in winnings. Limiting potential losses or ensuring gains, these orders automatically trigger the sale of an asset if it hits a defined price threshold.